You work for various reasons including to afford your life, bills, and acquire personal assets. Personal assets are the things you own that have value. They include land, personal property such as cars, cash, investments, and many more. There’s a lot of work that goes into acquiring personal assets. That’s why it’s very important to come up with a structure to protect your personal assets. One of the ways you can do that is by hiring professionals like those found on attorney Blake Harris website. If the topic of protecting personal assets is new to you, this article is for you. It looks at the benefits of asset protection and the various ways you can protect your personal assets. Keep on reading to learn more.

How To Protect Your Personal Assets

Below are some of the ways you can use as personal asset protection:

- Use Domestic Asset Protection

Sometimes, things may be challenging, and you get loans. Loans are helpful, but you risk losing your personal assets if you don’t meet your agreements when taking the loan. This is because creditors may acquire your personal assets to regain the money they lent you. Luckily, domestic asset protection protects your 4 Ways To Protect Your Personal Assets personal assets from creditors. This means your assets will be safe, and you’ll have the chance to pass your assets to your inheritors. Moreover, you may wonder if it’s necessary to protect your assets from creditors if you don’t have any outstanding loans. The answer is yes. No one is sure of how their tomorrow will be. You may find yourself in a messy situation, and your assets will be protected if you have domestic asset protection. In other words, domestic asset protection also protects your assets from future creditors you may have to deal with.

- Select The Right Entity For Your Business

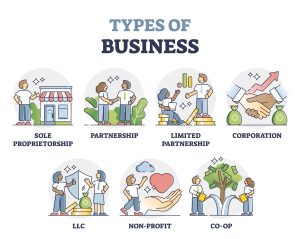

When starting a business, you must choose the structure you’ll use or what they called a business entity. There are various types of entities you can settle on. They include:

- Sole proprietorship

- General partnership

- Limited partnership

- Limited liability company (LLC)

- S Corporation

- C Corporation, and many more

When choosing your business entity, you should consider whether your personal assets will be safe or not. For instance, a sole proprietorship doesn’t separate your business from your personal assets. This means your business debts and losses may be deducted from your personal assets hence risk losing them. On the other hand, a business entity such as a Limited Liability Company doesn’t involve personal liability for your business’s debts. This means that despite your business’s performance, your personal assets will be protected. Furthermore, after choosing the correct entity, there are other factors you should consider for the protection purposes of your assets. These factors include:

- Have separate bank accounts. One for personal use and the other for your business

- Have different chequebooks

- Use your business’s name on documents, and

- Keep track of business records

Doing this will help differentiate what belongs to your business and what’s personally yours.

- Get Insurance Policies

Another way of protecting your assets is by purchasing insurance policies. There are several insurance policies you can use. Here are some of them:

- Malpractice Policy. In some careers, you can be held liable for malpractice. For example, in the medical field, you may have to deal with lawsuits and risk losing some of your assets in case of malpractice. However, with a malpractice policy, your personal assets are safeguarded if you lose a medical malpractice lawsuit.

- Umbrella Policy. You may have other policies already, such as homeowners’ policy, auto policy, and many more. However, in case of an accident, your policies might not take care of everything. For instance, you may be involved in an auto accident, and the court fines you $800,000. Your auto policy offers cap limits less than the fined amount. Your umbrella policy will cover the remaining amount in such a situation. As a result, your personal assets will be safe.

- Have A Prenuptial Agreement

Marriage is a beautiful institution. Unfortunately, every institution has its challenges, and marriage is no exception. At times, the issues in your marriage may lead to a divorce. Divorce cases aren’t easy to deal with as it involves factors such as:

- Dividing the assets that you have

- Alimony

- Tax consequences and others

Regarding assets division, it may be unfair to divide the assets if one partner acquired them. To avoid such an incident and protect your assets, it’s best if you have a prenuptial agreement with your partner. A prenuptial agreement is a contract between two people about to get married. This contract entails the assets owned by each person and how the assets will be divided in case of a divorce.

Benefits Of Protecting Your Assets

Below are the advantages you get when you protect your assets:

- You reduce the risk of being targeted by a lawsuit. Business creditors, at times, target your personal assets if they can’t benefit from your business’s assets. However, it’ll be hard for them to come after your assets with protected personal assets.

- You can retitle your assets. After a while, you may find the need to retitle your assets. It’s easy to retitle a protected asset as you’ll avoid cases of corruption or badges of fraud.

- You minimize conflicts with your business partners. At times, misfortunes may occur in a joint business and lead to losses. This means you’ll have to look for ways that you’ll use to recover. With asset protection, your assets will be safe as they’re not involved in your business.

- Fills in the gaps left by other policies. Policies limit what and how much they’ll cover in case of an accident. Unfortunately, if you’re involved in an accident that requires a lot more than what your policy can provide, you’ll be needed to find other means to fill in the gaps. Insurance coverage aims at asset protection to help in filling these gaps.

Summing It Up!

Based on the efforts you put in to acquire your personal assets, you should consider protecting them. Besides, there are other benefits of protecting your assets. For example, asset protection can help fill the gap that is left by policies that don’t cover very expensive assets. In this case, the asset protection will offer compensation. It also helps minimize conflicts in business and protects your assets from being repossessed by creditors. Therefore, if you’re considering protecting your assets, consider using these four ways discussed in the article.