When it comes to finances, what people pay the most attention to is either their savings or investments. But in order to increase your chances of being financially secure throughout adulthood, there’s another metric you should constantly strive to improve and protect: your credit score.

People’s credit scores are essential, especially in countries like the United States, the United Kingdom, and Canada where they play a big role in many aspects of adult life. Aside from it reflecting your financial history and habits, it’s also crucial when availing financial products such as loans and mortgages. The terms and factors behind what makes up your credit score vary from one country to another. That said, we will focus on the Canadian Credit Score for this guide. Curious About The Canadian Credit Score? Here’s How It’s Calculated

Overview

A credit score is a 3-digit metric used to identify borrowers’ potential to pay their loans or debts. The credit score range differs from country to country. For instance, in the UK, companies like Experian use a 0-999 point scale with 961-999 as the ideal score.

On the other hand, Canada’s credit system is similar to the United States’. Two of the US’s three biggest credit agencies, Equifax and Transunion, branched out to Canada and used the same criteria for identifying credit scores, which looks into factors such as payment history and credit utilization.

Equifax and Transunion branches in Canada use a 300 to 900 point scale. To get a reasonable interest rate, a borrower should have a minimum score of 680.

Credit Range

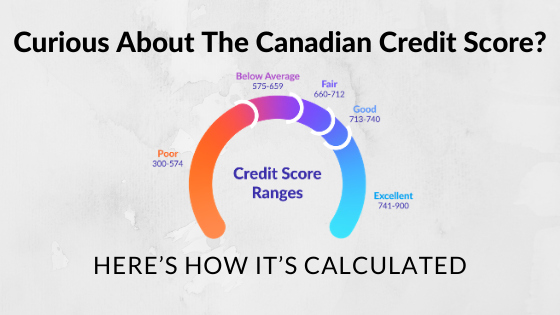

Before we discuss how credit groups calculate your credit score, here’s a quick breakdown of the credit score range in Canada as per the Equifax Risk 2.0 scoring model:

- Excellent (scores between 741 to 900): Consumers falling under this credit score range are guaranteed to get approved on their loans. They will also enjoy the lowest interest rates available, as well as higher credit limits.

- Good (scores between 690 to 740): Users with good credit scores can still be approved for loans, but will not likely to experience the lowest interest rates available.

- Average (scores between 660 to 689): Borrowers within this range will likely experience slightly higher interest rates from lenders. They may also not enjoy as many financial benefits from credit cards as they may still be ineligible for them.

- Below Average (scores between 575 to 659): Having a below-average credit score will not guarantee the approval of credit applications. Users will also face higher interest rates, which can cost them quite a lot of money in the long run.

- Poor (scores between 300 to 574): Users that have poor credit scores are likely to get their loan applications rejected. If you have this kind of score, you should seek financial handling assistance.

How credit companies calculate your credit score

Credit scores are just one out of the many, many things a lender considers when lending money to a potential borrower, but it doesn’t mean that we should neglect it. A high credit score means an individual can enjoy the best interest rates available on the market, which you can view using tools like Rate Genie. Meanwhile, those who have very low credit scores will likely get their new loan application rejected, and they’re advised to seek credit improvement help.

Credit agencies use elaborate systems to calculate every individual’s credit score. Here’s how they do it.

Equifax

Though it has the same credit score range as TransUnion, Equifax has a different way of calculating credit scores. The factors that Equifax considers may or may not be used by TransUnion as well, but each factor’s weight and influence vary.

Payment History: 35%

Payment history is a considerable chunk of the criteria, mainly because this reflects how a potential borrower manages and repays their debts. These debts may be in the form of the following:

- Credit cards

- Lines of credit

- Loans such as:

- Installment loans

- Auto loans

- Student loans

- Mortgage loans

All these payments are and will always be recorded regardless if you pay on time or not. Companies also take note of the ratio between your credit accounts and payment habits. For instance, your credit score may be affected if you have eight tradelines or credit accounts but only manage to pay four of them on time.

Credit Utilization: 30%

Every lender has a set credit limit or the maximum amount a borrower can lend. People commonly encounter the concept of credit limits when they’re applying for and using credit cards. This element plays a significant role in your credit score, especially when you’re already close to, at, or above your credit limit.

Taking credit cards as an example, you can get a lower credit score if your bank has set a $2,000 credit limit and you maxed it out. This caveat is due to the possibility of either not being able to pay it on time or not repaying it.

Credit History: 15%

Credit history includes the age of your credit accounts. In the credit score calculation, it mostly comprises both your oldest and most recent accounts. Creditors use this criterion to determine how you handle your credit accounts over time.

Public Records: 10%

Companies may also consider your public records when determining your credit score. For instance, your credit score can get lower if you have had collection issues in the past. Bankruptcy and other events that can generate a negative track record may lower your credit score as well.

Inquiries: 10%

Whenever you access credit files, it’s logged on as an inquiry. Inquiries that possibly affect one’s credit score include applying for a new credit card or asking for a credit limit increase. These hard inquiries imply that you might be facing financial problems or distress. Though this might not always be the case, companies take these hard inquiries and combine them with other criteria mentioned above. When these inquiries are verified, they can lower your credit score.

TransUnion

On the other hand, TransUnion uses similar criteria with Equifax, such as payment history, credit history, and credit utilization. Percentages are different, with the payment history having 40%, credit history with 21%, and credit utilization having 20%.

Here are the other criteria set by TransUnion:

Reported balances: 11%

The total number of recently reported balances can affect a borrower’s credit score. Balance reports are essential to lending companies who set automatic debit as their repayment option. This is why most lenders have penalty fees for NSF or non-sufficient funds.

New credit accounts: 5%

Similar to credit history, TransUnion gives importance to new credit accounts. Lenders usually prefer borrowers with older accounts as these accounts better reflect their financial handling. Of course, keep in mind that having older accounts doesn’t guarantee a high credit score. You can also focus on other factors like reported balances or even avail and maintain a credit card to increase your credit score.

Available credit: 3%

Not maxing out your credit limit can increase your credit score in Equifax, but that’s not the case with TransUnion. In general, try to keep your spending way below your credit limit.

How to improve your credit score

While there are some differences between Equifax and TransUnion’s criteria on credit scores, they are still quite similar. Here are some tips on how you can improve your credit score:

- Always pay on time: Paying your gazillion bills might be stressful, but you must always pay them on time. Some lenders don’t charge for pre-payments, so it’s better to take advantage of that since early and on-time payments can increase your credit score.

- Clear all outstanding debts: If you’re planning to apply for a loan, some lending companies will require you to pay all of your outstanding debts. This move can also influence your credit score significantly as having existing unpaid debts can make it lower. If you still have outstanding debts, it’s a reflection of your financial habits in general. (Zolpidem) It’s also good practice to pay every existing payable before applying for another loan.

- Apply for credit cards only when you need them: It might be tempting to get new credit cards in order to try to improve your credit score. However, having too many active credit cards might be detrimental to your credit score. For instance, having too many of them can prompt multiple inquiries on your credit status, which can ultimately lower your credit score. On a practical level, having numerous credit cards may also increase your spending and put you in debt.

- Always check your credit report: If you’ve received a credit report recently, make sure you check all the details included in it. Pay close attention to the numbers indicated there, as the wrong information can lower your credit score and affect your loans and other financial transactions in the future.

Conclusion

Having a good Canadian credit score is, without a doubt, essential to living a worry-free life. It’s also noteworthy that creditors use various pieces of information to determine a borrower’s financial capacity. The bottom line, however, is that as long as you manage your finances well, you’ll likely be able to cultivate a good credit score. Good luck!